Appropriately, we kicked off our new virtual Coffee and a Conversation series with a discussion about remote due diligence meetings, aka Zoom Diligence, and presented ideas for allocators who must now adapt their processes to harness the opportunities of a virtual environment. Here we summarize the key points from the conversation, including audience poll results and recorded snippets from the presentation.

Vidrio’s Brian Robinson, a former risk manager himself, drove the discussion. He kicked things off with a few questions for those at the table, followed by an insightful presentation that not only tapped into his previous experience, but also his recently unearthed passion for analyzing body language in remote settings.

Creating a Nexus of Due Diligence in the Age of Remote Meetings

While there may have been some initial reluctance to fully embrace virtual due diligence meetings as the "new normal," we’ve seen the industry quickly move past early concerns to realize the benefits of pivoting from onsite to remote visits. As our polls of the participants suggest, “Zoom Diligence” could be here to stay for many organizations, particularly given the cost and time efficiencies that many have experienced as a result of reduced meetings and related travel expenses.

Below:

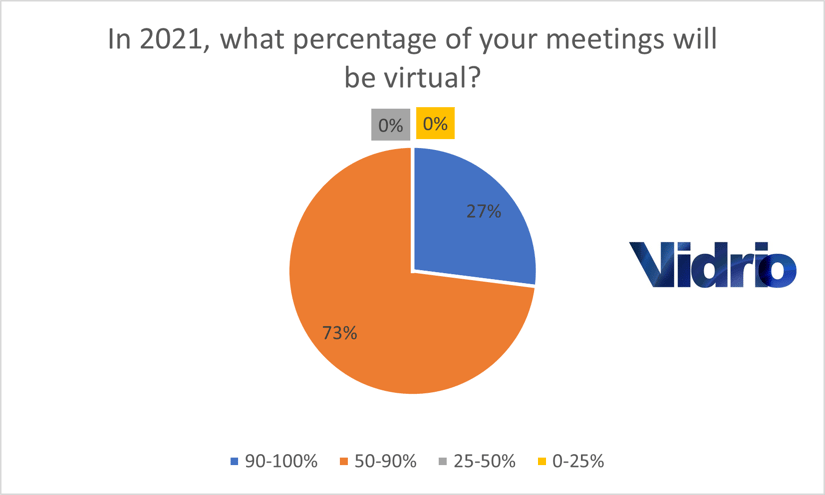

- Figure 1: 27% of our participants expect 90% – 100% of their due diligence meetings to be virtual in 2021, with the other 73% anticipating at least 50% to 90% virtual meetings.

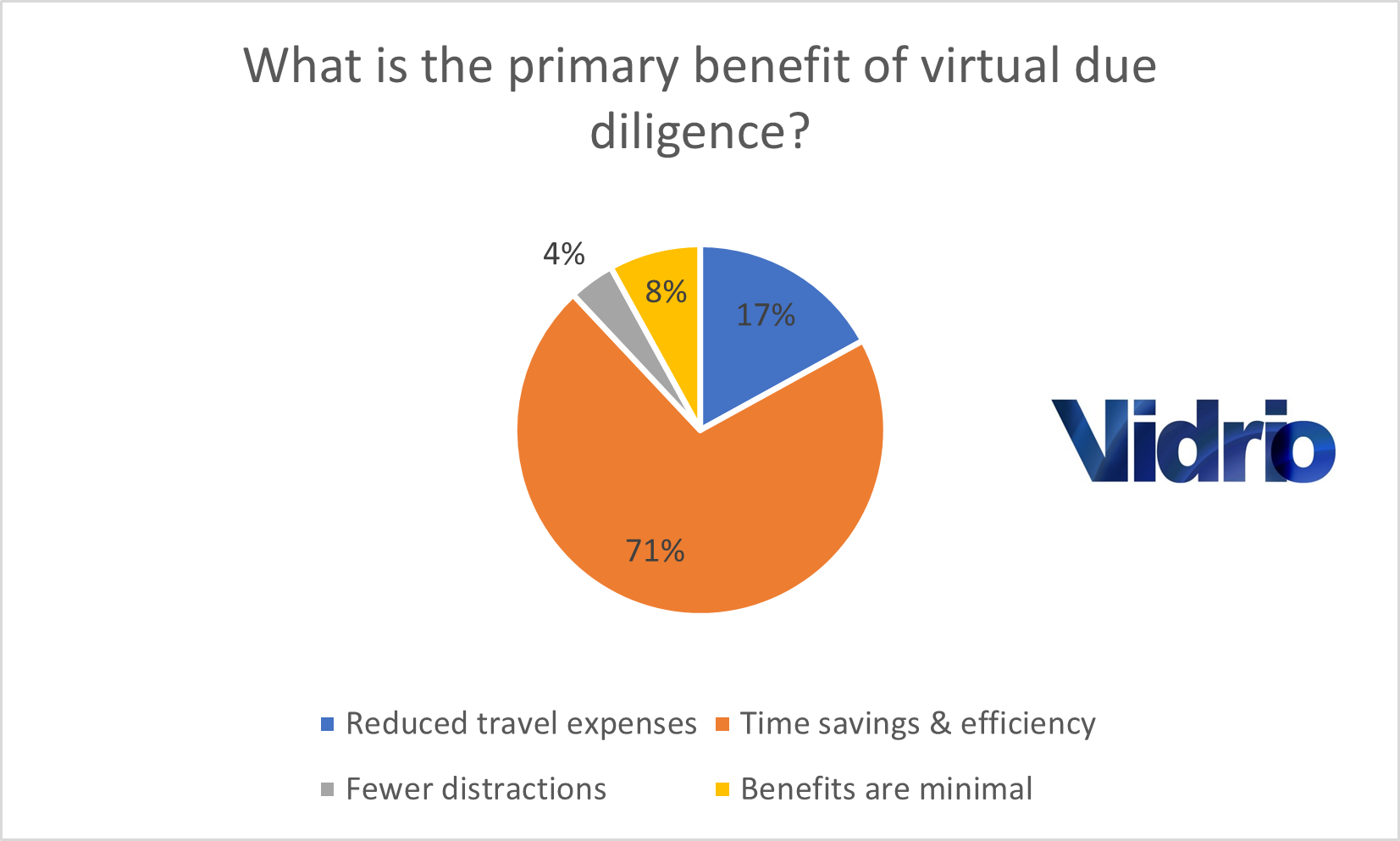

- Figure 2: 71% cited reduced time savings and operational efficiencies as the main benefit to virtual meetings, with 17% noting the reduced travel spend and 4% citing decreased distractions. Only 8% of the participants noted seeing minimal benefits.

Figure 1

Figure 1

Figure 2

Figure 2

Qualitative Due Diligence

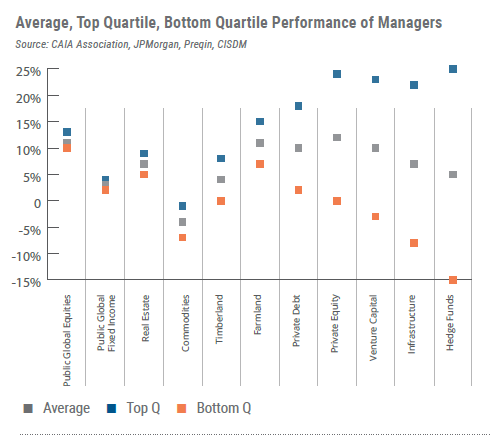

In their recent study, The Next Decade of Alternative Investments, CAIA shared a comparison of best and worst performing managers. As you’ll see in the below snapshot (figure 3), the report cites only a minimal dispersion between the top and bottom quartile for public equities. However, the dispersion amongst best and worst performing hedge funds is quite significant, with the top quartile showing +25% returns, while the bottom quartile had -15% returns. This indicate a 40% dispersion in the performance between the best and worst managers and underscores the significant impact that external manager selection can have on a portfolio.

Figure 3

Related to this, about 50% of our participants indicated that they are likely to allocate to a manager in 2021 that they have not previously met in person (figure 4).

Figure 4

Figure 4

So, what should a solid manager selection process look like in the age of remote meetings?

- Combine firsthand knowledge of managers with current information from reputable databases and be sure to capture in a centralized database/CRM.

- Become familiar with the latest “best practice” technologies and processes employed by fund managers and question those being vetted about their technology choices.

- Learn to read virtual body language (more on that below!)

The top priority in manager selection is, of course, to avoid fraudulent managers with a rigorous vetting process that holds up whether done virtually or not. This can be best achieved by combining firsthand knowledge of specific managers with information from reputable databases such as HFR, Eurekahedge, etc. The use of such databases can enhance the process by helping to identify managers and strategies that meet specific performance and risk criteria.

Ideally the above knowledge and information would be brought into a centralized database and/or CRM alongside contact bios, relevant documentation, meeting notes, communications, fund terms and assets under management. This approach is proving to be particularly valuable in 2020, where the new trend among many allocators is to only “shop their closet,” meaning they are only allocating to managers with whom they have previously invested, or at minimum, have previously met before in person. Those allocators with a comprehensive database of vetted managers will find it easier to adjust to this approach.

That said, even the most fully vetted managers from previous years may not have transitioned well to the current environment, so some previous managers aren’t going to be suitable options for future allocations.

What then?

Regardless of the current circumstances, Allocators need to be able to look for new managers for investment, and double down on both background and reference checks in the absence of in-person interaction.

As part of this process, allocators will want to vet potential new fund managers with the following questions, and be equally up to speed themselves on the latest technologies and processes used by fund managers:

- What technology is the manager currently using? When was it last updated? Hint: “Excel and email” are not optimal answers.

- Is the manager using multiple technology systems? If so, how closely do those systems integrate?

- And related to the above, how does data move between their different technologies, systems, and processes?

Understanding Virtual Body Language to Avoid Fraud

As Brian discusses in the below recording, the ability to learn and understand different mannerisms, analyze communication styles, and generally get a strong “gut reaction” is considerably hindered when meeting someone in person is not an option. Studies show that only about seven percent of words spoken by a presenter contribute to the listeners’ opinions of that speaker, while their body language contributes more than half. Of course, trying to get a read of body language “on screen” is significantly more challenging.

For instance, it is much easier to be charmed by someone via videoconference. With so many slouching and seemingly disinterested participants succumbing to video fatigue, it is easy to be lured in by someone who simply makes eye contact and sits up. So, beware of the easy charmer and any bias toward liking them, and follow these tips from Brian to help assess trustworthiness in a virtual environment:

- When posing a question, take note of the manager’s eyes and/or head movements. Do they shift to the left or to the right?

- Right is recall, left is lying.

- The opposite is true for left-handed people.

- And keep in mind that virtual environments create a mirror effect, where left is right, and right is left…so take this one with a grain of salt!

- Notice the manager's shoulders.

- Like a dog’s tail, shoulders can give a good read of comfortability.

- Raised shoulders shows tension.

- Face-touching is an indication of self-soothing and could also indicate nervousness/tension.

- Wait five minutes for a person to become comfortable. If they don’t, their ongoing tension could be a cause for concern.

- Conduct reference checks, and be speak to multiple members of the fund management team – not just the person presenting.

- When all else fails, ask more questions than one might normally ask in person and avoid making certain assumptions. Less is not more in this scenario.

Psychopathic Tendencies and Performance

In one of the more captivating moments of his presentation (which you can view around minute 4:20 in the above recording), Brian summarized a psychological case study previously presented at a past CAASA event. The study was originally published by Leanne ten Brinke, Aimee Kish, and Dacher Keltner in a 2017 Personality and Social Psychology Bulletin.

The researchers collaborated with numerous asset managers to review videos of over 100 manager due diligence meetings. In doing so, they were searching for signs of a “triad of bad behaviors” that could indicate psychopathic behaviors, including:

- A lack of empathy

- Uncaring behavior toward others

- A willingness to do anything to get ahead.

Prior to the study, there was a strong perception that the above personality traits made for high performing traders or managers. As it turns out, the results of the study showed just the opposite. When comparing returns, Managers who displayed certain psychopathic behaviors underperformed consistently. This was attributed to those managers being unwilling to admit bad investments and to cut losing positions. The study also showed that their personality traits lead to their treating their staff poorly, which in turn leads to high turnover (hence tip #3 above re: speaking with team members and conducting reference checks).

Quantitative Due Diligence - Follow the Money

While the bulk of the conversation focused on qualitative due diligence, which has been the most impacted by a move to virtual meetings, Brian also mentioned a set of quantitative due diligence practices worth noting here, which are important whether in a virtual or in-person environment.

To summarize:

- Follow the money line with a view on cost of doing business vs. firm AUM

- Build workflows for forecast expectations matched to underlying assets in the portfolio

- Remember that distressed debt, credit, or co-investments are far less liquid than large caps, which means it could take a lot longer to liquidate your positions in these assets.

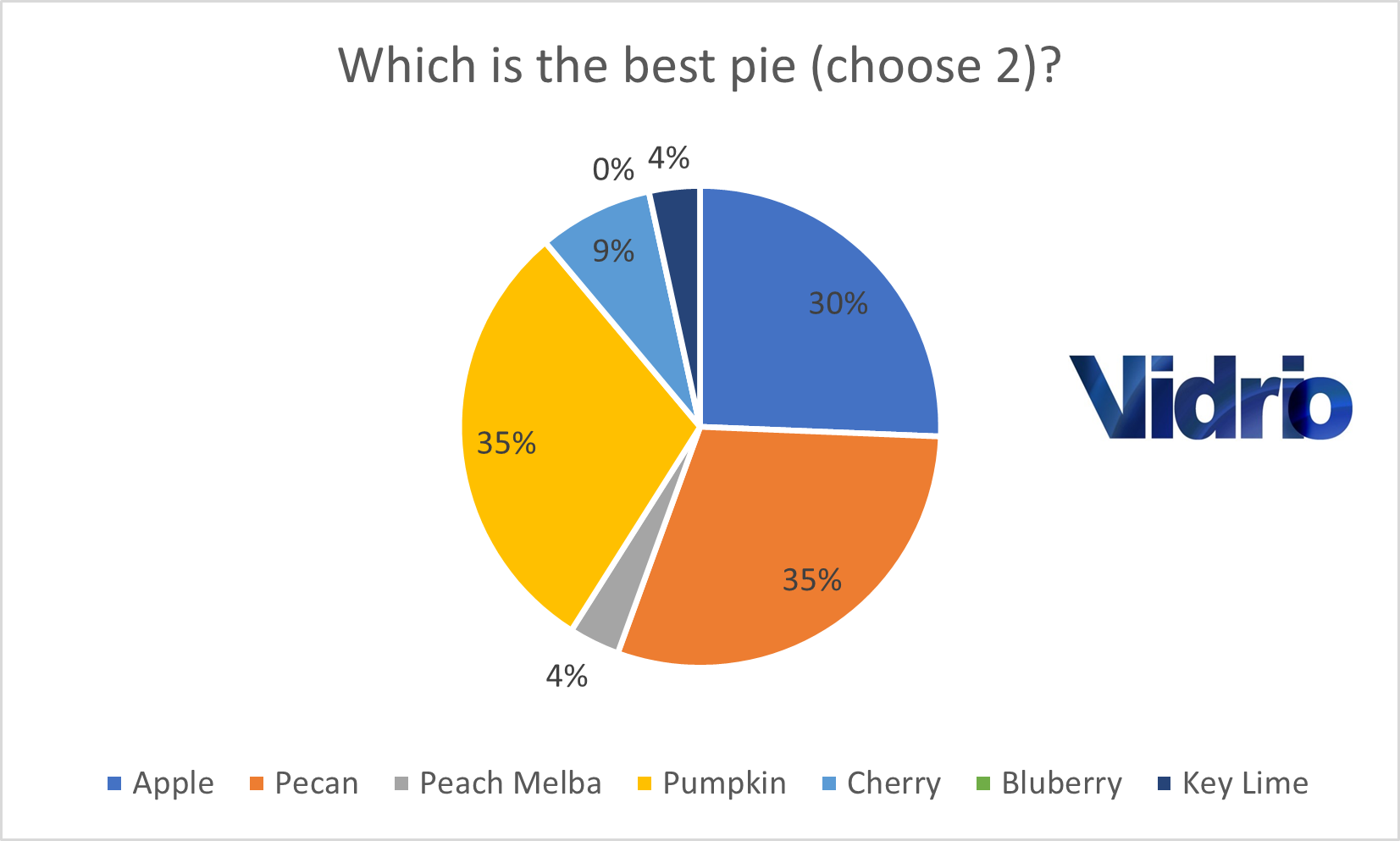

A Pie Chart About Pie

And finally, for those of you who like a side of pie with your coffee, we are pleased to share the results of our fourth and final question to the audience, in the spirit of last week’s Thanksgiving holiday. Alas, no love for the blueberry.

Many thanks to all who participated in this first conversation of the series. It was great to see so many of you at the table, and we look forward to the next Coffee and a Conversation.

Figure 5

Figure 5

Ready for the New Normal?

During 2020, your processes most likely changed, and rather quickly. It is critical to reflect on what you are doing differently now, to assess how/if those changes have impacted the effectiveness of your due diligence approach and whether or not your organization still has the right systems and technology in place to support your evolving processes in the long term.