In our latest Coffee and a Conversation, Vidrio's Willett Bird met with Kamal Suppal, Chief Investment Auditor of the Boston-based, Emerging Markets Alternatives. The two discussed the nuances of conducting due diligence on private market funds/managers, with a focus on the current virtual environment and best practices that allocators and LPs should consider during their research processes. Following is a summary of the conversation and a link to stream the audio recording.

Due Diligence of Private Market Fund Managers - Nuances and Trends

In an era marked with many moving parts and growing uncertainty, our guest speaker, Kamal Suppal stressed, "past in no longer prologue,” and “ we are in an epochal phase in our investing careers," where asset allocators need to look at every investment through a new lens and consider investment opportunities (and risks) via a more multi-dimensional framework. Kamal emphasized that lower global economic growth, rich valuations and rising correlations in public markets creates the need to push boundaries and seek more idiosyncratic returns within the Private Markets.

However, it is first important to understand the nuances of researching private market funds and managers during the due diligence process, as outlined here:

- Opacity: Private Markets are opaque, and allocators can’t get away by selecting brand names or selecting strictly on historic fund performance. It is important to lift the hood and do a very granular analysis of everything at an individual deal or transaction level. When pursuing risk premiums in Private Markets, first determine: What is the source of alpha? Where is the manager getting the premium from, e.g., through some propriety knowledge? Some network? Origination capability? Regulatory arbitrage? Also, What is the margin of risk: Potential upside/downside scenarios? What if the manager gets it wrong?

- Sustainability of Alpha: Does the investment strategy have a long runway or short window of opportunity? Take Sustainable Mining, for example, where something like the emergence of resource nationalism could emerge to place restrictions on where a particular company can/cannot mine and import resources, and suddenly an entire investment thesis is out the door.

- Ability to Execute and Extract Alpha: Does the manager have a repeatable, consistent process to extract Alpha? Are their processes nimble enough to adapt to changing circumstances and do they have the appropriate and agile deal teams in place?

- Responsible Execution: Is the manager following the tenets of sustainable finance and thinking holistically for all stakeholders, or are there signs of “green washing?”

Green washing, or “SDG washing,” refers to instances of managers claiming alignment with ESG or Sustainable Development Goals, without making practical efforts to actually achieving the goals. To avoid this, investors will want to ensure that the manager’s "responsible" processes are truly integrated within the investment framework, including the pricing of climate risk.

- Sound and Stable Operations: In relation to the above investment processes, does the manager demonstrate a commitment to sound and stable operations? Are there investors incentivized to stay for the long haul? Is there evidence of stable AUM? Are they operating above break even? Are they utilizing reliable service providers?

- Complete Alignment Between LPs and GPs: It is important that the GP demonstrates a strong willingness to maintain a constant, open dialogue with the LP. There must be a symbiotic relationship: Remember that GPs need LP’s capital as much as the LP relies on the GP to expertly execute and tap into new opportunities. The economic relationship (e.g., management fees) should be structured to ensure fairness to both sides with complete transparency on expenses, valuation practices, key man provisioning and all other disclosures that are necessary to ensure the LP is well-protected.

Adaptation of P/E Due Diligence to Remote/Virtual Environments

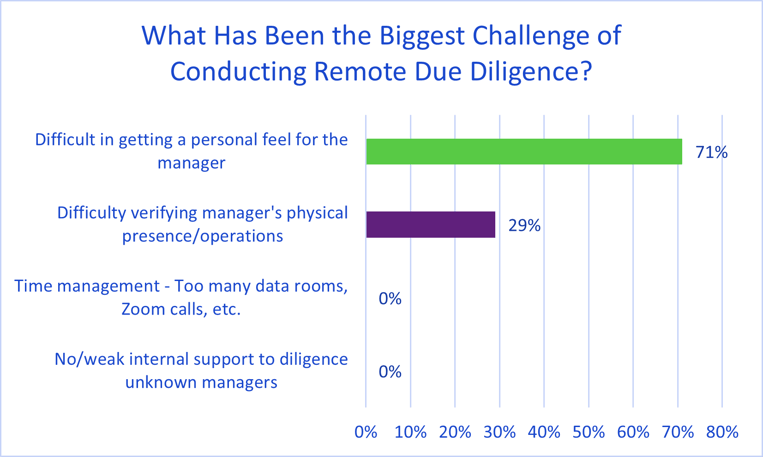

It came as no surprise that our audience flagged manager assessment and team dynamics – getting a personal feel for a manager – as the primary challenge of conducting due diligence in the current remote environment. We are more than a year into the Pandemic, and it's likely fair to say that “Zoom Diligence,” as Vidrio has coined it, is here to stay for the long run, along with other interesting trends as we enter year two of the virtual world.

As Kamal commented, while there is certainly screen fatigue all around, the flipside is that businesses are seeing strong efficiencies from virtual capabilities, including an increase in productivity, more organized and agile teams, and of course the elimination of redundant travel and related expenses.

Further, asset owners are now being exposed to interesting new investment opportunities. Some specific examples outlined by Kamal include SaaS/Mobility ventures in emerging markets such as India and Southeast Asia to middle market lending in Asia where investors can still enjoy premiums with investments into data centers, e-commerce facilities in real estate, digital infrastructure, etc.

Efficiencies and opportunities aside, investors are still not willing to pull the trigger on certain allocation decisions with managers that they’ve not met in person. So how can allocators adapt and get comfortable with remote due diligence to leverage meaningful opportunities within their portfolios? “Adapt or perish,” says Kamal.

Enabling P/E Due Diligence for Allocators and LPs

As Kamal reinforces, we will be in a virtual environment for the long term and adaptation is the name of the game. Allocators must be willing to adapt a change in mindset and think outside the box to address the current situation.

- Build new core competencies. While “diligencing” of traditional private markets "managers" (e.g., Private Equity, VCs, etc.) has long been in practice, current times call for building core competencies in understanding geopolitics, domestic policies and ESG, as well as an understanding of the CFO's office, etc. It might also require that allocators consider reorganizing their research teams into silos of expertise where people are not just asset class specialists, but also learn to specialize in the undercurrents that now flow through all opportunities and asset classes. The understanding of these factors and their impact on investment theses are more crucial than ever to any due diligence.

- Look within your own portfolios to cross-pollinate ideas. What do you own and whose insights can you leverage to get local insights? For example, when trying to diligence high performance assets in India, it is important to get a sense of private sector vs. public sector banks in the region, bankruptcy law, etc. It might help to identify an equity long/short manager within your portfolio who might be investing in Indian banks and request insights into the local landscape. Or as another example, if looking at resource-efficient tech in Europe, reach out to an energy infrastructure manager for their insights, and so on.

- Seek support from due diligence specialists. While some of the ideas articulated in the discussion might be a complete departure from what many allocators are used to, and indeed may sound radical, Kamal advises that allocators strapped for time and resources should not be shy about seeking expert help and outsourcing diligence to due diligence specialists who might be hard-wired to think more holistically and may be able to leverage local networks and offer clinical assessments of opportunities and risks without non-investment and administrative tasks clouding the analysis .

- Broaden your scope and best practices. In the absence of being able to meet in person, it is important to widen the scope of investment checks. Allocators should consider who they know in common with the managers they are researching. Speak with ex-employees, follow the money: How does it go in and out of the manager? Become more familiar with body language and understand the cultural differences in body language to avoid misreading certain physical cues. And befriend technology – be willing to move beyond cookie cutter spreadsheets to leverage software and analytics that enable the slicing and dicing of information to perform and maintain a record of both qualitative and quantitative due diligence. Know what you are looking for and work with providers that can customize solutions to analyze individual managers and opportunities more adequately.

- Prepare, prepare, prepare. Before jumping onto a Zoom call, allocators must prepare in order to be in control of their conversations. With adequate preparation, one can direct the flow of the conversation to ensure the desired information is obtained, vs. what the managers want to give.

To sum up all the above: Due diligence in today’s environment is a journey, not an event – it is imperative that allocators and LPs can adapt to the new investing era with a multi-dimensional approach.

Facilitating Private Markets Due Diligence

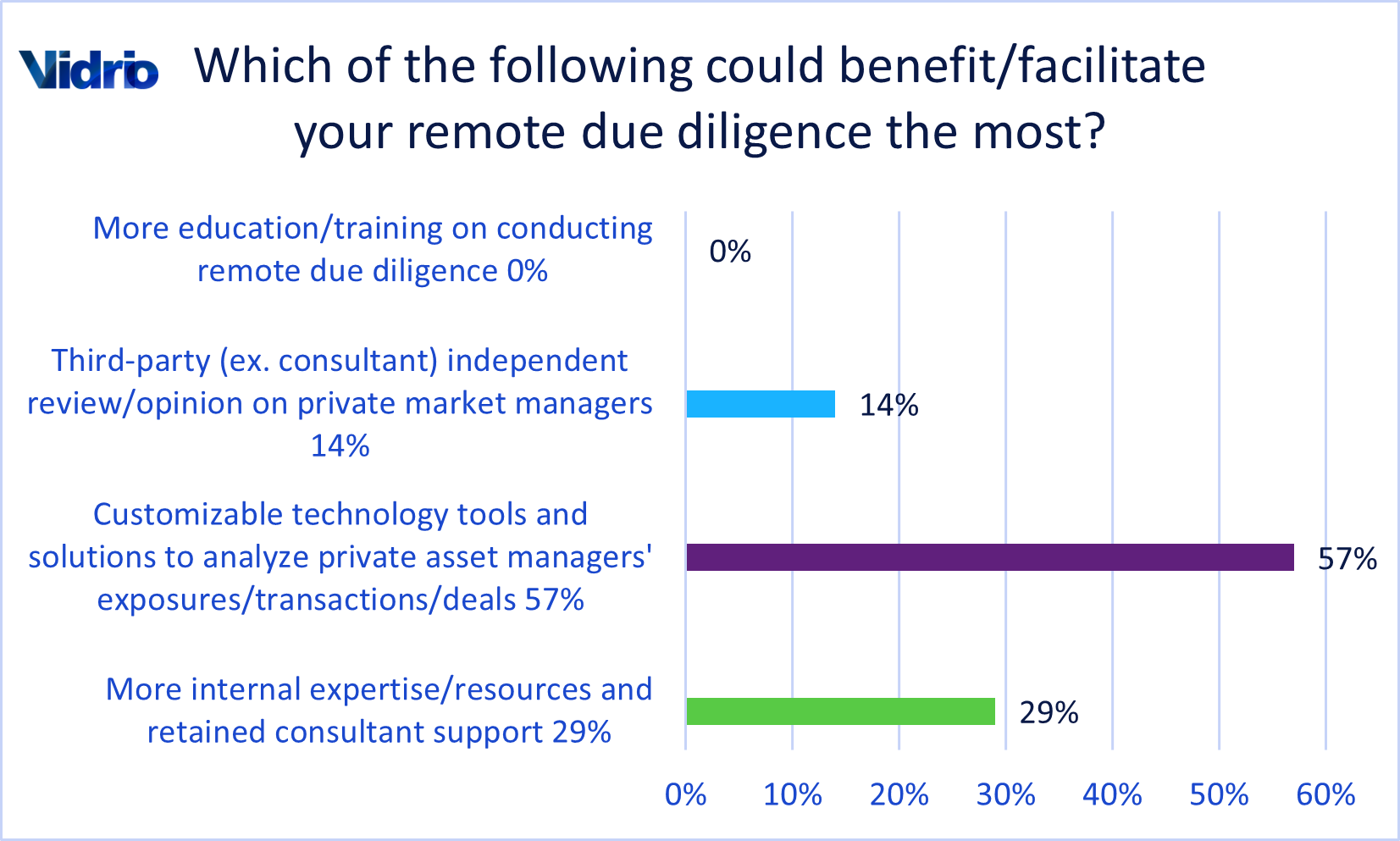

Over half our audience flagged customizable technologies and tools as a solution that everyone could benefit from. While we at Vidrio are of course pleased to see this corroborated, we are not surprised. Over the last 12 months, we have increasingly heard from our own clients and other allocators and LPs that their ability to conduct top-down analyses and see a complete picture of exposures, transactions, deals, etc. is more crucial than ever before – across all asset classes, both private and public.

In addition to the benefits of SaaS, any asset owner strapped for time and resources can still conduct a very objective assessment of the investment opportunities that they are researching. There is also great benefit to be had from external Investment Audits – an innovative service that Kamal launched through his firm, Emerging Markets Alternatives. More recently, the firm has launched a due diligence enabling service, Virtual Intelligence, which overcomes current (and even future) travel challenges of conducting due diligence by sharing with investors, a video recording of a virtual onsite with a manager, offering complete insight into a manager’s investment thesis and execution that investors can leverage to qualify a manager for further due diligence. The concept of Investment Audits is partly inspired by Kamal’s drive to democratize research and due diligence for investors, and inspired by the EU’s MiFID II rules, which have created a whole new industry in independent research and could potentially find its way to the US in due course. Similar to a financial audit, an investment audit enables allocators and LPs who might otherwise be strapped for time and resources to gain a 360 degree independent evaluation of an alternative strategy/manager. Read more about Emerging Markets Alternatives and their unique approach to independent investment audits.

Audience Questions

Following is a summary of questions that were posed to Kamal at the close of the conversation. Please contact ksuppal@emaltsauditor.com or willett.bird@vidrio.com if you’d like to follow up on any of the points discussed in the audio recording or summarized here in this blog post.

Q1: How do you ensure that virtual onsite is not a forum for a manager pitch?

A1:We do a lot of pre-work before doing a virtual onsite. Post our initial interview of the manager , weget into their data room, review all available documentation, and then seek customized responses and transaction level data All that pre-work then culminates intothe virtual due diligence meeting where all that has been learned can be verified, clarified and walked-through. Iwithout any scope for the manager to deliver a product pitch.

Q2: What does risk management look like in long duration assets during what Kamal called the “apocryphal” phase?

A2: There are two aspects:

- Illiquidity – when investing for the long haul, there can be a lot that can go wrong from the initial investment to when the investment thesis comes to pass and/or mature.

- It depends on where/what is underlying the investment. There are a lot of external forces at play that can be outside the control of the manager, as all investments are subject to a lot of moving parts. For example, we increasingly find government playing an influential role in many investments (e.g., infrastructure), and a lot is predicated on how privatization takes place, what policies are enforced, how pricing is regulated, etc.

To sum it all up: Time duration and all these external factors could ultimately influence the opportunity.

Q3: How do you verify authenticity of private market deals from a manager’s track record?

A3: What Kamal and his team do on behalf of their clients, is not just look at fund level information, but really, “rip apart” all the funds, extract individual transactions and collate the information that follows the entire deal life-cycle of every deal from start to finish. They then identify sample transactions based on materiality to a manager’s performance and manager’s business, and seek (virtual) face time with the manager’s counterparties, e.g., borrower/ investee company, to conduct one-on-one closed-door sessions that not only establish authenticity of deals and parties, but also to understand why and how they chose to transact with that manager vs. other choices. This also gives further insights into the manager’s execution from the other side of the aisle.

***********************************************************************************

While the above summary hones in specifically on the discussion points related to private markets due diligence, Kamal started this conversation with a broad illustration of forces that are reshaping a new investing era with implications for global capital markets. You can listen to the complete audio recording via the link below.

Intro - Geopolitical and other factors impacting the global investment strategies

09:45 - The Case for Private Markets

13:30 - Due Diligence of Private Market Fund Managers - Nuances and Trends

20:45 - Adaptation of P/E Due Diligence to Remote/Virtual Environments

31:45 - Enabling P/E Due Diligence for Allocators and LPs

***********************************************************************************

About our Speakers

Kamal Suppal, CFA is Chief Investment Auditor of the Boston-based, Emerging Markets Alternatives, which specializes in independent research and due diligence of alternative strategies executed by emerging managers in developed and emerging markets. His research - with a bias toward private market strategies - is for the benefit of global institutional investors.

Willett Bird, CFA is Director of Business Development at Vidrio Financial - a complete front- to middle-office investment management solution with integrated data services, sophisticated analytics and business controls for institutional allocators and LPs across the globe. Vidrio’s data aggregation and analytics help solve complex fund management problems, improve operational efficiency, and reduce risk for multi-asset-class portfolio investors. Our clients are the world’s premier allocators to external managers.