Will hedge funds be a tough sell for institutional investors in 2024? What are some of the latest opinions on the use of artificial intelligence from both hedge funds and other allocators? Vidrio brings you some quick takeaways from the Pension Bridge Europe event.

By: Ralf Papen, Executive Director, Vidrio Financial

How are fund managers proving their skillset to consistently deliver alpha in light of asset allocators looking to protect their portfolios from market volatility, inflation, geopolitical concerns, and more? In hopes of gaining even greater intelligence on these themes, Vidrio Financial journeyed to the With Intelligence, Pension Bridge Hedge Europe event, (Zurich, Switzerland) in early February. The event helps to bring European hedge fund leaders into the spotlight for networking opportunities and panel discussions with institutional investors, consultants, and family offices. Our takeaways follow below.

The Hedge Fund Perspective:

Hedge Fund perspectives on performance ran the spectrum of opinions throughout the event. Many in attendance believed that hedge funds that followed larger trends or macroeconomic factors around certain asset classes would quickly regain favor with institutional investors. However, these opinions were swiftly dismissed due to the underwhelming performance observed in the prior year. Several attendees further countered that hedge funds continue to be a tough sell for investors, getting punished for being more liquid than other asset classes, and when the performance started to tank, many managers were forced to liquidate. The more positive trend throughout the Pension Bridge Europe event was that European allocators are asking for more customization in hedge fund investments, looking for:

- Specific volatility profiles.

- Single managed accounts (SMA) structures.

- Flexible share classes.

- Better offering terms.

- Seeding hedge fund

- In-house managed accounts.

The cautionary tale here was that although customization ranked high with allocators, everyone in the institutional investing space needed to be aware of the risks associated with geopolitical disruption for at least the next 12-18 months. Unfortunately, this is something that is clearly unavoidable around the world and is sadly becoming the new normal in considering future portfolio scenarios and investments.

From a Vidrio perspective, we have seen a bit of the opposite trend taking shape. Hedge funds are still very much in favor, posting 2023 gains worth close to $220 billion after fees, according to a report by LCH Investments via Observer. Names like Citadel, D.E. Shaw, Millennium Management and Bridgewater Associates all topped the list of percentage return on investments, gaining 10.5% in 2023, beating the industry average of 6.4%. We believe that these hedge fund leaders will continue to draw attention (and allocations) from institutional investors across pensions, endowments and foundations, family offices, SWFs, and others as we progress into 2024.

From a regulations perspective many event attendees believe that larger hedge funds (specifically those in the top 20) will face greater scrutiny moving forward due to unfavorable terms and larger fees. This will leave allocators to search out more small-mid size hedge funds with better performance numbers. The larger regulatory concern here is that many hedge funds could face being categorized as systemically important financial institutions (SIFIs) if regulations were to increase. A SIFI is typically synonymous with a bank, insurance company, or other financial institution that could pose a risk to the economy if it were to collapse. The term in the United States for classification purposes is “too big to fail”. Unlike banks, hedge funds don’t have the resources to meet stricter SIFI guidelines as it relates to holding more capital, liquidity risk limits or standards, portfolio stress testing, and more.

There’s also a level of transparency that is up for debate as well as it relates to the SIFI designation. The fear is that there could be two different AUMs being reported, one with leverage and one without. For the one with leverage, most likely going to regulators, many could infer that the fund is too big to fail and thereby calling for the SIFI designation. Vidrio agrees with the opinion that this could drastically increase operating costs and suppress more innovative managers and fewer allocator choices over the longer term.

The New Investing Buzzword: Uniform Portfolio Management:

Naturally there are a lot of buzzwords in the institutional investing space and especially some that overlap with the way Vidrio assists allocators in navigating their data challenges and portfolio monitoring needs.

Some that immediately come to mind are transparency, a single source of data truth, red flags, and more. While at the Pension Bridge Hedge Europe event many attendees focused on the need (and keyword) of improved uniform portfolio management. This term, according to those that we spoke with, has been gaining traction across various allocators as a critical need for a standardized approach to managing investment portfolios. This approach, when applied in the correct context emphasizes consistency, efficiency, and scalability in the management of institutional investment portfolios. The conversations around these topics further emphasized the following aspects:

- Standardization of the investment process.

- Efficiency and scalabiity.

- Risk management.

- Regulatory compliance.

- Client communciation.

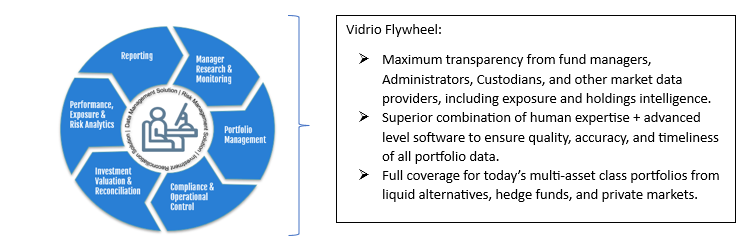

As asset allocations and portfolios become more complex, these types of methodologies will become more prevalent, driven by a mix of human expertise and advanced software solutions. Frequent visitors to the Vidrio website, or part of our digital communications community, will certainly recognize the Vidrio flywheel that incorporates all these aspects in a single flywheel design. Be sure to schedule your demo with our team today if you find your methodology across these key aspects lacking in any way.

Common Ground on Artificial Intelligence for Funds and Allocators:

From the need for better portfolio solutions, the discussions turned to another buzzword: Artificial Intelligence for institutional investors. Many allocators are struggling to define what their use case is for artificial intelligence and whether they build an internal model, (similar to MassPRIM Developing AI Model to Aid Investing) or go the outsourcing route. In the case of MassPRIM, AI could be used (in theory) to assist with future investment decisions, based on decades of prior investment data. Many at Pension Bridge Europe believed that machine learning or AI tools could most certainly help with the efficiency of front, middle, and back-office operations but stopped short in saying that large language models should get involved with actual trading. Vidrio Financial agreed with most of the coverage on the usage of AI as we’ve been an early pioneer leveraging advanced neural networks and deep learning across our own platform solution. You can read more about our work from our Q2 blog entry on Harnessing the Power of Artificial Intelligence for Institutional Investing from early last year.

We enjoyed our time at the With Intelligence Pension Bridge Europe event and look forward to future installments of these discussions. If you’re eager to delve deeper into Vidrio Financials’ partnership options available to asset owners and managers, please don’t hesitate to reach out to us through our website. We would be delighted to guide your team through our demo environment, tailor a plan to suit your objectives, and help you achieve/accelerate your investment goals.